By NIKO LEHMAN-WHITE and SAEED AMINZADEH

Introduction

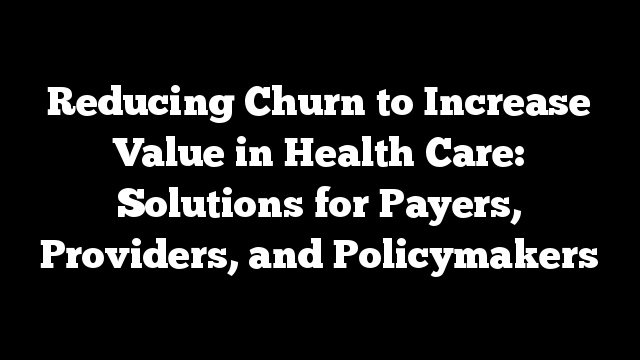

Every day and in every corner of the country, innovative health care leaders are conceiving of strategies and programs to manage their patients’ health, as an alternative to treating their sickness (see Figure 1).

The value-based contracts that have proliferated in this

country over the past decade and which now account for about half of the money

spent on healthcare allow these wellness investments to make good financial

sense in addition to benefiting patient health.

However, a phenomenon in health coverage in the US is

increasing costs, destabilizing care continuity and holding back the potential

of value-based care. It prevents us from making the long-term investments we

desperately need.

Understanding Churn

Churn refers to gaining, losing, or moving between sources of coverage. Every year, approximately a quarter of the US population switches out of their health plan. Reasons can be voluntary or involuntary from the perspective of the beneficiary (see Table 1) and vary from changes in job status, eligibility, insurance offerings, and preference, to non-payment of premiums, to unawareness of pending coverage termination.

Table 1. Examples of

reasons for voluntary and involuntary disenrollment from a health plan

| Voluntary Disenrollment | Involuntary Disenrollment |

| Decided too expensive | Forgot to sign up |

| Decided to forego coverage | Lost eligibility |

| Newly eligible for public insurance | Couldn’t afford premiums |

| Moved | Passed away |

| Want a different network | Confused by application process |

| Unhappy with insurer |

A study by the Center for Healthcare Research and Transformation asked Michigan policyholders whether they continued with the same plan they held the previous year. 72% of those surveyed with employer-sponsored insurance (ESI) stayed on plan. 62% of Medicaid beneficiaries did. Only 47% of those who purchased coverage on the individual marketplace kept their plan the following year.

Implications for care

and cost

Churn’s impact on medical care and quality is far greater than most realize. It impacts medication use (over 33% of individuals experiencing churn skip doses or stop taking a medication altogether) and often forces consumers to change doctors (primary care provider, specialist, or both). Patients with coverage interruptions have higher Emergency Department use, more hospitalizations, more serious mental health problems that lead to hospitalizations, and delays in the screening, detection and treatment of cancer. Churn also contributes to higher administrative costs.

It also disincentivizes long-term investment. Food-as-medicine

programs like Geisinger’s Farmacy, housing investments, and asthma programs make

less financial sense when a patient’s policy has a looming expiration date.

This issue is far less problematic in nations where

universal health insurance programs are offered. Since these programs will

likely cover a person for their entire life, they know that an investment in

wellness made at age 20 will still pay dividends when they’re 80 (an age which

they are more likely to reach because of those investments), which is one

reason why we see higher levels of funding for social programs in these

countries.

That situation differs drastically from the US, where

insurers know that most policies will be held for only a year or two and before

any investment has a chance to be returned, its target population will have

churned into another plan and their expensive investment ends up helping their

competitor. Thus, churn damages the financial return for the exact long-term

investments we need to make to improve health and decrease healthcare costs.

What follows are recommendations for changes that providers,

payers, and policymakers can make to minimize the impact that churn has on

their constituents and financial health.

Payers

One strategy that payers can use to combat churn is to focus

on engagement. Losing enrollees is expensive, and less engaged enrollees are

more likely to disenroll from their health plan. To truly move the needle in

today’s market, payers must be proactive and utilize sophisticated targeting

methods. A targeted retention program can be effective in minimizing this loss

if several guiding principles are followed.

- Pick the right members. Some members are simply higher risk to voluntarily disenroll than others. A “one size fits all” marketing campaign targeted to every member with the same message will not provide the best results. The cost of this type of campaign will likely not be sustainable for the results it achieves. For an effective, efficient campaign, leveraging insights from a high-performing predictive model which predicts the likelihood of voluntary disenrollment is essential.

- Try to understand why members might disenroll. Targeting the right members based on their likelihood to leave the plan is a great way to zero-in on the highest risk members. However, it’s knowing why these members will leave the plan that can help your organization to personalize the communication to these members. Otherwise, the organization risks missing the true barrier that the member is facing in terms of staying on plan. Keep in mind that members don’t necessarily leave because they’re unhappy with the plan: they might leave because they don’t understand or see the value in their current plan. In short, try to identify and resolve or address issues for members that are dissatisfied, and try to get the unengaged member to better engage with the health system.

- Stay ahead of network changes. If a member is high risk to leave the plan and you already know that you’re going to make changes to the network in this patient’s service area, try to stay ahead of this issue and address these issues upfront. Consider ways to explain in plain English the reason for the change, your commitment to their service area, and the various options available to the member. Any other type of communication to these members will result in making their flight risk higher, not lower.

- Try to coordinate member outreach with other plan initiatives. The end of the calendar year also signals a push for other important plan initiatives. Coordinating across teams in the organization is critical for reducing the number of outreaches any one member receives. If a member is in need of outreach for multiple initiatives (for example, staying on plan and undergoing a regular cancer screening), then either prioritize one of the communications or modify the communication outreach to avoid overwhelming the member.

- Know that this is a journey. Reducing voluntary disenrollment is satisfying from both a return on investment perspective and from a quality perspective. However, it’s important to know that this is only a first step. Now you can continually engage the member who was at high risk of leaving the plan to create longer term loyalty with the plan. Year-round “touches” and check-ins with members signals an understanding of the members’ challenges and begins to transform the plan from a “claims payer” to a “trusted source of information” in the eyes of the member.

Providers

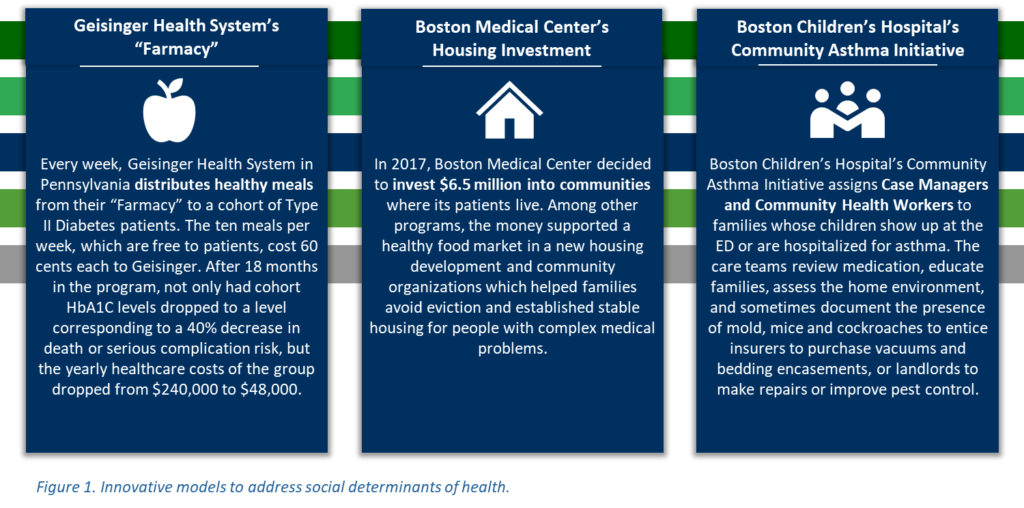

A strategy that providers can deploy to defend against churn is to treat a patient’s eligibility date as a vital sign and proactively address an upcoming potential lapse in coverage, just like they proactively address an anticipated heart attack. Some innovative providers now consider health insurance status as a social determinant of health given the resulting likely disruption to continuity of care and downstream impact of that disruption to patient outcomes. By integrating a patient’s eligibility date with traditional data in, for example, an electronic health record (EHR), providers can trigger a low intensity intervention to keep the patient enrolled on plan and his or her care undisrupted (see Figure 2).

Some of the strongest support cases for this work has been completed by a group at Oregon Health & Science University (OHSU) whose body of published literature reads like a summary of our recommendation to providers (e.g., “Improve Synergy Between Health Information Exchange and Electronic Health Records to Increase Rates of Continuously Insured Patients”, “Health information technology: an untapped resource to help keep patients insured”).

Expanding inclusion of social determinants of health in the

EHR could be accomplished by developing new workflows to gather data, building

new data fields into the EHR, and creating linkages to other existing data sources.

Although the work at OHSU targeted state Medicaid-enrolled patients, patients

enrolled in individual marketplace plans, in Medicaid and Medicare Advantage

plans, and in ACOs could all benefit from clinic-based efforts to maintain

insurance coverage.

State and Federal Lawmakers

and Policymakers

Policymakers also have levers at their disposal to reduce

churn. This can be done in public insurance programs like Medicaid and CHIP,

and through individual market regulation.

Half of the US Medicaid population will lose their coverage within 12 months of signing up. This churn can have a particularly adverse effect on children, who are enrolled in Medicaid and CHIP in high numbers, frequently interact with the health care system, and take time to build trusting relationships with their caretakers.

Churn is especially prevalent in Medicaid because its eligibility is determined by month-to-month income, which tends to vary significantly in the low-income population covered by the program who frequently transition in and out of jobs. Eligibility determinations add another layer of complexity. Work requirements as a condition of Medicaid eligibility, which some states have proposed or implemented as a way to increase civic participation and reduce Medicaid enrollment, will further contribute to churn not only because of noncompliance with the requirement, but also because of confusion and technical difficulty with submitting proof of civic engagement. Only 1,525 of the 69,041 beneficiaries subject to Arkansas’ new work requirement program (imposed in May 2018) both complied with and accurately reported data for their 80-hour-per-month mandate.

Several contributors to public payer churn have nonpartisan

solutions. Many enrollees stumble during the renewal process, so Medicaid

programs would do well to automate the process or simplify renewal forms and

translate them into appropriate languages. Some suggestions to have included:

- Express lane eligibility: Use data from other benefit systems such as SNAP or TANF to determine Medicaid eligibility.

- Continuous eligibility: When someone enrolls, keep them on the program for a minimum amount of time (usually 12 months).

- Administrative verification of income: Make the government verify income eligibility, rather than requiring beneficiaries to submit proof.

- Consumer assistance programs: Develop programs that assist people with eligibility and enrollment questions.

- Increase government incentives to practice in underserved areas and accept publicly funded insurance: Limited geographic access and long wait times decrease the value of health coverage. Increasing access for the underserved will make Medicaid coverage more worthwhile to consumers.

- Annualized income determination: Assess income on a yearly basis rather than monthly, to reduce the impact of income fluctuations.

Federal policymakers can address churn in individual and

SHOP markets by allowing carriers to decrease their premiums or cost-sharing for

consumers who renew an individual or small-group plan they held the previous

year. This is already common practice in auto and home insurance policies. Allowing

state insurance commissioners offices to bestow this “incumbent price

advantage” in health insurance would require a change to the Affordable Care

Act, which only allows plan prices to vary individually based on age, smoking

status, and location. This proposal would pose a barrier to entry for new carriers,

so the competitive ramifications of any “price break” policy should be fully

evaluated by a state before being allowed.

Conclusion

Churn has vexed insurance executives for decades and is considered by many at this point an inevitable challenge. But now that the value-based movement has led to a refocusing on social determinants of health, incentives are aligned to address this issue. This solution may be a key step towards a healthcare system focused on investing in health rather than in treating illness.

Niko has a background in research and consulting and enjoys writing about and solving problems facing the US health care industry.

Saeed has more than 25 years of health information technology experience, with a track record of building high-performing organizations designed to solve complex business problems.